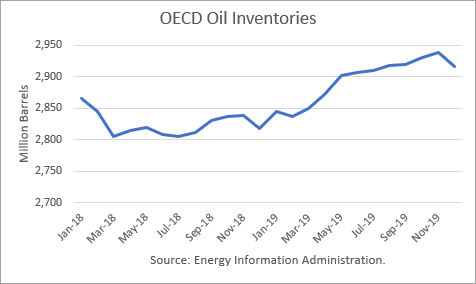

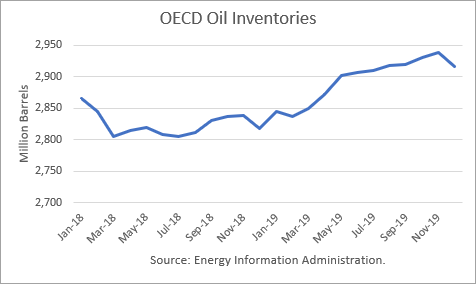

The Energy Information Administration (EIA) released its Short-Term Energy Outlook for October, and it shows that OECD oil inventories likely bottomed in July at 2.806 billion barrels. It shows inventories rising in the third quarter, contrary to the normal seasonal trend. However, it forecasts that stocks will drop in December to 2.817 billion after the Iranian sanctions are expected to go into effect.

Throughout 2019, OECD inventories are generally expected to rise, ending the year with 98 million barrels more than at the end of 2018. The expected drop in Iranian production, due to the U.S. sanctions, is forecast to be more-than-offset by increases from other producers, such as the U.S., Canada and the Gulf states of Saudi Arabia, Kuwait and the UAE.

Crown Prince Mohammed bin Salman of Saudi Arabia has recently stated that KSA can produce at least 12 million barrels per day. If it does increase output to that level, this would be a major “surprise” to world markets since its production has never exceeded 11 million.

The moment of truth is near: how much of Iran’s production and exports will be cut, and will that loss be offset? We will know soon, as the new sanctions go into effect in early November. If Vitol’s chairman is correct, there is an abundance of oil available, and the price escalation is fear-based.

Oil Price Implications

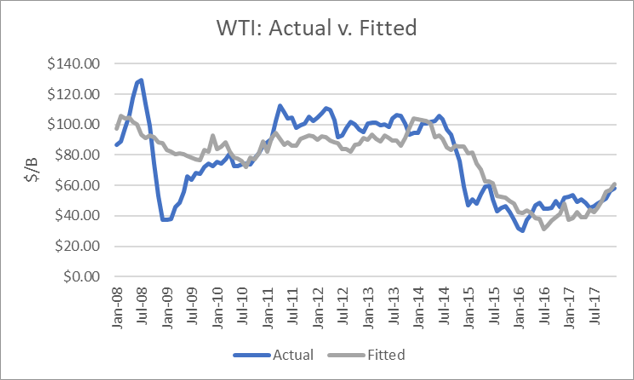

I performed a simple linear regression between OECD oil inventories and WTI crude oil prices for the period 2008 through 2017. As expected, there are periods where the price deviates greatly from the regression model. But overall, the model provides a reasonably high r-square result of 79 percent.

I used the model to assess WTI oil prices for the EIA forecast period through 2019 and compared the regression equation forecast to actual NYMEX futures prices as of October 12th. The result is that oil futures prices are overvalued. Later in 2019, oil prices would drop into the low $50s if these inventories are realized.

Conclusions

The outlook for production, stocks, and prices is particularly risky in both directions. However, current market conditions indicate no impending shortfall, and I expect the Saudis will fulfill their pledge to make up for losses from Iran’s production and exports.

Looking further into the future, I expect that the U.S. will renegotiate the nuclear agreement with Iran and receive the terms it has demanded because Iran’s economy is suffering and there is a risk of “regime change” to the current leaders should that occur. Such a development would put an end to sanctions and allow Iran to increase its exports once again.

I also expect that the NOPEC legislation in the U.S. will pass Congress and be signed into law by President Trump. The effect would be to make foreign oil-producing countries subject to the Sherman Antitrust Act, prohibiting restraint of trade or collusion on pricing or production, if they want to do business in the U.S. Such a development would effectively terminate OPEC’s ability to control production to achieve higher oil prices.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor – Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.