Considering new monetary policy frameworks and the case of Japan, Part 1: Raising the inflation target and price-level targeting

After the Global Crisis of 2008-09, many central banks in advanced economies faced the effective lower bound and thus found it necessary to implement unconventional monetary policy to achieve an inflation target of around 2%. Unconventional monetary policy tools include large-scale bond purchases, stock purchases, negative interest rates, forward guidance on policy rates, yield curve control, and cheap lending facilities conditional on banks’ lending to the private sector. Over the past years, the effectiveness of such policy has been increasingly questioned given that many central banks have struggled to raise underlying inflation (i.e. inflation excluding volatile food and energy). In response, the search for a better monetary policy framework is increasingly becoming one of the main topics among central banks. Before the Global Crisis, central banks formed a consensus that flexible inflation targeting– which attempts to achieve around 2% in the longer run by taking into account resource maximisation – is a main pillar of the monetary policy framework.

Factors contributing to the search for a new monetary policy framework

This consensus has become somewhat shaky since the crisis for three reasons. First, the neutral rate of interest has declined since the early 1990s for structural reasons (i.e. ageing, declined productivity growth, global savings) and cyclical reasons (i.e. the legacy of the crisis) and is highly unlikely to recover to the pre-crisis higher level. This suggests that the nominal policy rate will remain lower than in the pre-crisis period, thereby generating a higher probability of falling into the effective lower bound again when a next crisis or recession happens. For example, the nominal federal funds rate in the US is likely to be around 3% or lower, compared with around 5% before the crisis.

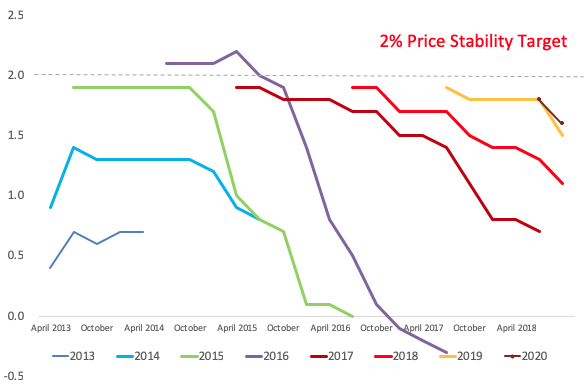

Second, the effectiveness of unconventional monetary policy on inflation has been increasingly questioned. While these innovative tools have helped to lower long-term yields, depreciate exchange rates, and raise stock and real estate prices, their impacts on inflation and inflation expectations have not been as strong as central banks had initially hoped for. For example, it took the Federal Reserve more than six years (since its adoption of the 2% goal) to achieve about 2% based on personal consumption expenditures (PCE) and core inflation in March 2018. For the ECB, inflation based on the harmonised index of consumer prices (HICP) reached around 2% from April 2018, but core inflation has remained around 1%- well below their price stability target of “below, but close to, 2%.”The Bank of Japan (BOJ) failed to achieve the 2% price stability target over the past five years since Quantitative and Qualitative Easing (QQE) (Table 1). According to the latest August 2018 data, CPI-based inflation recorded 1.3% but CPI excluding all food and energy was mere 0.2%. Figure 1 shows that the BOJ’s inflation projections have been persistently optimistic so that it was forced to make downward adjustments almost steadily over time as the end of the fiscal year approached with the release of actual data.Until March 2018, moreover, the BOJ claimed that the timing to reach 2% inflation is around fiscal year 2019 after having already postponed it six times. In April 2018, the BOJ finally dropped the claim and gave up expressing the timing to reach 2% inflation – a clear sign of losing confidence in achieving the target soon.

Table 1 The Rate of Change in CPI in Japan

Note: Excluding the Direct Impact of the Consumption Tax Hike

Source: Ministry of Internal Affairs and Communications

Figure 1 BOJ’s inflation projection (medium of the board members’ projection)

Source: Bank of Japan.

Third, adverse impacts of unconventional tools – such as market price distortion, mounting household debt, declined banking sector profitability, adverse impacts on pension and insurance industries, quasi-fiscal policy, and inequality – are increasingly becoming apparent. These costs may exceed the aforementioned benefits if such tools are in place for too long.

In an attempt to cope with these concerns, central banks increasingly feel more comfortable with traditional monetary policy tools (i.e. using a policy interest rate) due to familiarity with their effectiveness. In such circumstances, there has been a growing focus on alternative frameworks such as (1) raising the inflation target (for example 4% rather than 2%), (2) price-level targeting, (3) nominal GDP targeting, and (4) nominal wage targeting. This column focuses on the first two frameworks.

Raising the inflation target as a new monetary policy framework

Raising the inflation target enables a central bank to maintain a highernominal policy interest rate in normal times, thereby enhancing its ability to use a traditional monetary easing tool (Blanchard et al. 2010). Nonetheless, this framework has lost traction, especially among central banks with well-anchored inflation expectations for fear of dis-anchoring them.

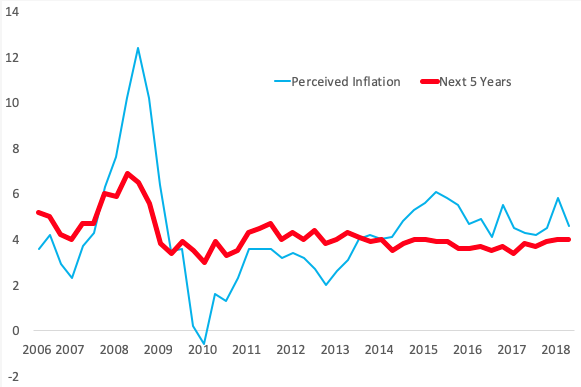

For Japan, adopting a higher inflation target seems politically difficult since there is little public support for the 2% price stability target. The lack of support arises from the fact that households consider prices of goods and services to have been high and expect they will be high. Figure 2 indicates that households’ perceived rate of inflation (a rate of current perceived price change as compared to one year ago) as well as long-term inflation expectations(over the next five years) have remained not only positive but also very high. This occurred even when the rate of actual CPI-based inflation was negative in 2009–2012 and 2016. This is a reflection of the fact that not only has households’ real disposable income has not only risen since early 2000s, but also that their income expectations have remained sluggish and unchanged (Shirai 2018a). Due to tighter household budgets, their spending has been very sensitive to the prices of daily goods and services. A recent example is the January–March quarter of 2018, when a contribution of consumption to real GDP growth turned negative due to higher food prices caused by bad weather.

Figure 2 Japan’s perceived inflation and inflation expectations (%)

Source: Bank of Japan.

Price-level targeting as a new monetary policy framework

Price-level targeting, which theoretically is more powerful than inflation targeting, has been gaining traction among some central banks and academics. This is because price-level targeting attempts to maintain stability of the price level along the desired long-term price level path (constructed, for example, assuming that the 2% inflation rate is always achieved) by making up thepast deviation ofactual prices from the path (i.e., mistakes)– while flexible inflation targeting ignores the past deviation of actual inflation from the 2% inflation targetand attempts to achieve 2% inflation going forward. Therefore, a central bank’s monetary policy response is history-dependentfor price-level targeting and is history-independentfor flexible inflation targeting. If actual inflation remains low for many years, for example, a central bank should achieve higher-than-2% inflation for a while to bring actual price levels back to the desired price level path, and vice versa. If the public are rational and forward looking (so that they fully understand the desired path as well as a central bank’s attempt to make up for the past deviations), their long-term inflation expectations will likely be more firmly anchored at around 2% as compared with flexible inflation targeting.

In its 2011 review of the flexible inflation-targeting framework, the Bank of Canada examined price-level targeting as a possible option but concluded that the benefits did not outweigh the risks of dis-anchoring inflation expectations and thus losing central bank credibility (Bank of Canada 2011). Some hold the view that price-level targeting could be a potential option in the US – including adopting it temporarily, only when the effective lower bound prevails or flexibly by introducing the ±5% range around the price level path – since it may strengthen the effectiveness of forward guidance on a policy interest rate with greater forward commitment (Evans 2012, Williams 2017, Bernanke 2017, and Bostic 2018). So far only one economy has implemented price-level targeting – Sweden experimented with it for less than two years when it went off the gold standard in 1931 (Mester 2018).

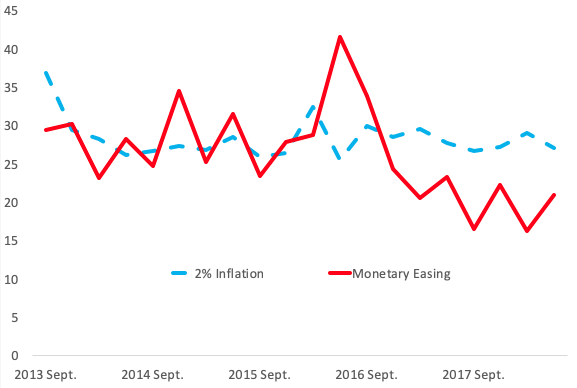

In the case of Japan, price-level targeting has rarely been brought into discussions. This is mainly attributable to the BOJ’s failure to promote communication with the public about its policy objectives and thus to achieve inflation toward the 2% inflation target over the past five years (Figure 3), as well as households’ resistance to price hikes. As a result, the deviation of actual inflation from the 2% price level (starting from 2013 when the official 2% inflation target was adopted) has not only widened but has also been much wider than in the US (starting from 2012 when the 2% longer-run goal was explicitly adopted), as shown in Figures 4a and 4b. Reaching the price level path is an extremely difficult task for the BOJ due to the limited effectiveness of the current monetary easing tools for generating inflation. The idea of trying to generate a rate of inflation exceeding 2% for many years to achieve the price level path is unlikely to be accepted by the public.

Figure 3 Japan’s awareness of the 2% inflation target and monetary easing

Source: Bank of Japan.

Figure 4 Desired long-term price level path and actual price level

(a) Japan (2012=100)

(b) United States (2011=100)

Source: Statistics Japan; Federal Reserve Bank of St. Louis.

Conclusions

The search for a better monetary policy framework has received a lot of attentions in recent years. A number of alternatives have been put forward with the objective of achieving price stability more firmly in the low neutral interest rate environment. But such discussions are rare in Japan because of the public’s limited understanding of the 2% price stability target and people’s resistance to higher prices. There is a widespread view that the BOJ should lower the price stability target to around 1% or even abandon the target altogether. This seems to be widely supported by the public. Very few forecasters believe that inflation will reach 2% in a stable manner in the foreseeable future. According to the latest June 2018 ESP Forecast Survey conducted by the Japan Center for Economic Research, for example, the average projection of forecasters (excluding the direct impact of the consumption tax hike) recorded only about 1% in 2020-24 and 1.2% in 2025-2020.

My view is that the BOJ should introduce flexibility in interpreting the 2% price stability target. It should incorporate the 1% upper and lower range (±1%) of the target into the 2% target itself.The BOJ and the government would then not need to abandon the 2% target while in practice aiming at a 1% figure that would be acceptable to the public. Such flexibility would be better than lowering the target from 2% to 1% since many central banks have begun to interpret the 2% price stability more flexibly. For example, Sweden’s Riksbank adopted ±1% target range into the 2% target in 2017. Eric Rosengren, the President of the Federal Reserve Bank of Boston, has suggested an adoption of an inflation range (1.5-3%) in the US since a rate of optimal inflation may be uncertain and unfixed like the natural rate of unemployment (Rosengren 2018). Moreover, a scheduled increase in the consumption tax in October 2019 from 8% to 10% is expected to generate inflation above 2% for a year. That gives officials the opportunity to introduce a 1% to 3% inflation target range that could be easily presented to the public. The BOJ may eventually find discussing the appropriateness of the inflation target and an appropriate monetary policy framework (including normalisation of monetary policy) inevitable. This is likely to happen during the second term of Mr. Kuroda’s governorship

References

Bank of Canada (2011), “Renewal of the Inflation-Control Target: Background Information—November 2011”.

Bernanke, B N (2017), Monetary Policy in a New Era, Peterson Institute for International Economics.

Bostic, R (2018), “View on the Economy and Price-Level Targeting”, Federal Reserve Bank of Atlanta, 21 May.

Blanchard, O, G Dell’Ariccia and P Mauro (2010), “Rethinking Macroeconomic Policy”, IMF Staff Position Note SPN/10/03.

Evans, C L (2012), “Monetary Policy in a Low-Inflation Environment: Developing a State-Contingent Price-Level Target”, Journal of Money, Credit and Banking 44: 147–155.

Mester, L J (2018), “Panel Remarks on the FOMC’s Monetary Policy Framework”, remarks at the 2018 U.S. Monetary Policy Forum, New York, 23 February.

Rosengren, E S (2018), “Reviewing Monetary Policy Framework”, Remarks at a Forum on the Federal Reserve’s Inflation Target, Hutchins Center on Fiscal and Monetary Policy, 8 January.

Shirai, S (2018a), Mission Incomplete: Reflating Japan’s Economy (Second Revision), Asian Development Bank Institute.

Shirai S (2018b), “BOJ’s Huge Stock-Buying Program Reaches its Limits”, Opinion, Nikkei Asian Review, 21 September 21.

Williams, J C (2017), “Preparing for the Next Storm: Reassessing Frameworks and Strategies in a Low R-star World”, FRB Economic Letters 2017-13: 1–8.